The last year seems to have tested the patience and skills of the Middle East’s hospitality sector. A recent report by TRI Consulting titled The Middle East Hotel Market Review revealed that hotel performance levels across the Middle East remained static or declined during 2016, largely driven by lower oil prices, reduced government and private sector spending and the ongoing political and civil problems in the Levant. Many hoteliers were forced to lower room rates to maintain market share, leading to a rate war along with a negative effect on profits and RevPAR.

However, the forecast for 2017 is positive on multiple fronts. TRI’s report shows that most markets will either bottom out or slowly start recovering as oil prices stabilise, key infrastructure projects come online and new tourism strategies take effect. This is also compounded by the fact that the hotel industry in the Middle East, and particularly in the GCC, is one of the fastest growing markets in the world.

Similarly, according to Alpen Capital’s GCC Hospitality Industry 2016 report, despite the slowdown in 2016, the market is likely to recover in the long-term, driven by the strong pipeline of hotels, with government efforts and events pushing tourist numbers up. Overall, the market is expected to grow at a 7.6% CAGR from an estimated US $25.4 billion in 2015 to US$ 36.7 billion in 2020.

The report revealed that during the forecast period, occupancy rates at hotels and serviced apartments are anticipated to grow by three percentage points to 70% and ADR is likely to average between $168-190, growing 1.4% annually. As a result, the aggregate RevPAR of hotels and serviced apartments in the GCC is projected to grow at a CAGR of 2.3% to $133 by 2020.

So what does this mean for hoteliers, and how does it impact recruitment, training, as well as salary? And does the potential improvement in the hospitality sector mean that hoteliers are keen to stay where they are, or look for new opportunities?

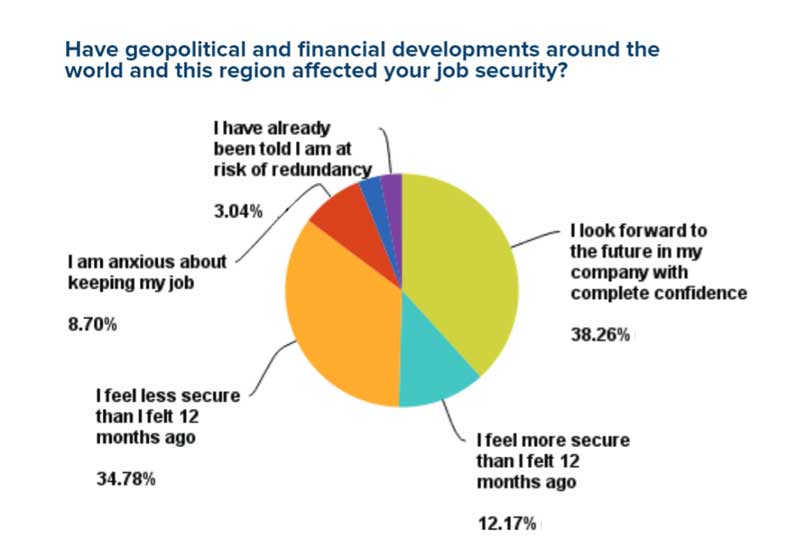

MOVING AHEAD?

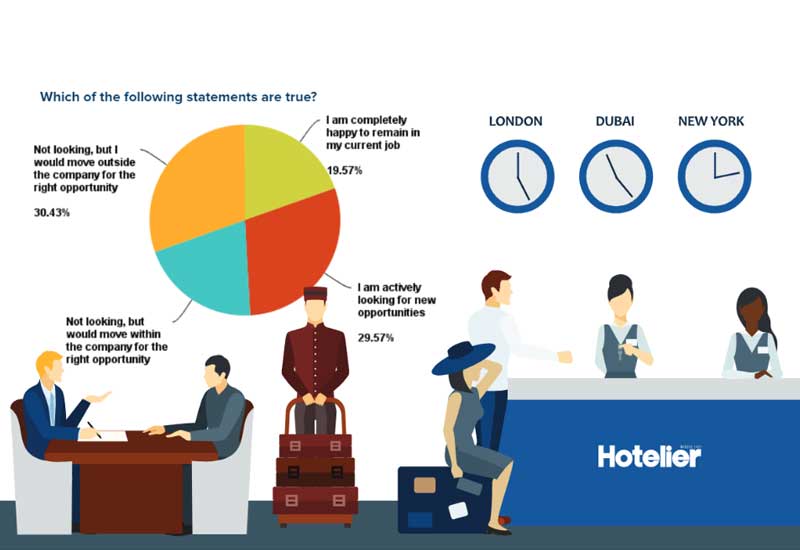

Nearly 30% of our respondents have said that they are actively looking for new opportunities, while nearly 20% have categorically stated they are happy in their current roles. The remaining 50% have said they are not actively looking, split into 20% who wouldn’t mind moving for the right opportunity within the company, and 30% who would move outside their company if the right opportunity came along.

The percentage of people actively looking for new jobs wasn’t a big surprise for Samir Arora, who is the general manager of The Retreat Palm Dubai, MGallery by Sofitel. He told Hotelier Middle East: “This is always the case in buoyant situations where demand is more than supply. Qualified associates know that there are many new hotels opening and will have ample opportunities in this scenario. Furthermore many are here in this part of the world to better their salaries and careers. New hotels are offering incremental salaries to attract quality personnel from the same market in order to have an edge over the others to find their feet in the market.”

This is backed up by The First Group’s (TFG) recent whitepaper titled ‘The Impact of Staff Turnover on a Hotel’s Income Statement’, which revealed that approximately 28,000 new hotel rooms are expected to come online in Dubai by the end of 2018, reflecting an average growth rate of 12.5% per annum (John, 2015). On that note, 110,000 new jobs are anticipated to go live in the sector in the run-up to 2020 (Bouyamourn & Sahoo, 2014).

All well and good, but that means hoteliers have new opportunities to try, which makes retention a challenge. In the UAE, based on this report, employee turnover is approximately 25-30%. Additionally, the reasons revealed behind turnover included: career advancement in other hotels; better compensation offered elsewhere; lack of training; poor relationships with colleagues and/or managers; job security; lack of engagement; and, stronger brand values. So how do we retain staff?

| Advertisement |

Search our database of more than 2,700 industry companies

Search our database of more than 2,700 industry companies

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}